Bristow S-92 returns to Aberdeen in the early afternoon sunshine on 11th March 2020.

OPEC++

How many times have we all used the word ‘unprecedented’ in the last few weeks? Just when you think things can’t get any further from normal…. they do.

For anyone expecting drama today, the OPEC meeting certainly didn’t disappoint. Speculation during the day had seen the price of a WTI barrel fluctuate between $25 and $28 during afternoon trading ahead of the announcement. Far from the lofty heights of $61 seen on the first day of the year but a positive double-digit percentage improvement on the $20 seen at the start of this month. In the days leading up to the meeting there had been speculation that a cut of as much as 15 million barrels per day in April could be agreed.

In the opening statement of the OPEC meeting, the Secretary General stated “Given the current unprecedented supply and demand imbalance there could be a colossal excess volume of 14.7 mb/d in the 2Q20. This oversupply would add a further 1.3 billion barrels to global crude oil stocks, and hence exhaust the available global crude oil storage capacity within the month of May.” The implication here was clear…. either act now or see oil prices plummet further and perhaps even go negative when storage becomes full.

A cut of 10 million bpd is well beyond anything OPEC has arranged previously. In other words…. unprecedented! Perhaps less than some in the market had been expecting, however, and oil prices fell to $23/bbl as the extent of the deal became clear to the market late on Thursday 9th April. A further 5 million bpd is expected to come from producers outside of the OPEC + group with a call due on Friday 10th April between G20 energy ministers.

This isn’t a silver bullet for the oil industry’s problems. Demand destruction has been so severe that it is likely that oil storage facilities will still continue to see inventories rise in the coming months. Estimates of current demand vary but most suggest that more than 20 million bpd of demand has evaporated leaving a huge gulf between supply and demand that the OPEC deal will narrow, but not fully close.

Why does any of this matter? From a rotorcraft perspective, surely cheap oil is good, right? After all, it’ll take 2,877 litres of fuel to fill a standard S-92. However, for rotorcraft working on offshore crew transfer, fuel costs are in most cases passed through to the end customer at cost. The end customer is most likely an oil company, and oil prices determine revenue which impacts the free cash flow of an oil company. At $60 oil, most of the majors had significant free cash flow and expectations at the start of the year were for an increase in investment.

In short: Higher oil prices = more investment offshore = more offshore crew transfer activity.

How can oil companies respond in a low oil price environment? Aggressive cost cutting, both in terms of operational cost (OPEX) and capital expenditure (CAPEX). The problem offshore is that new projects often run into the billions or even tens of billions of dollars and can take years from final investment decision (FID) to first oil. At FID, contracts for construction and procurement of long lead-time equipment are awarded and walking away from these contracts is very expensive. When the oil price falls, oil majors therefore look first to discretionary expenditure (including well workovers and non-essential maintenance) and greenfield projects that are not yet past FID.

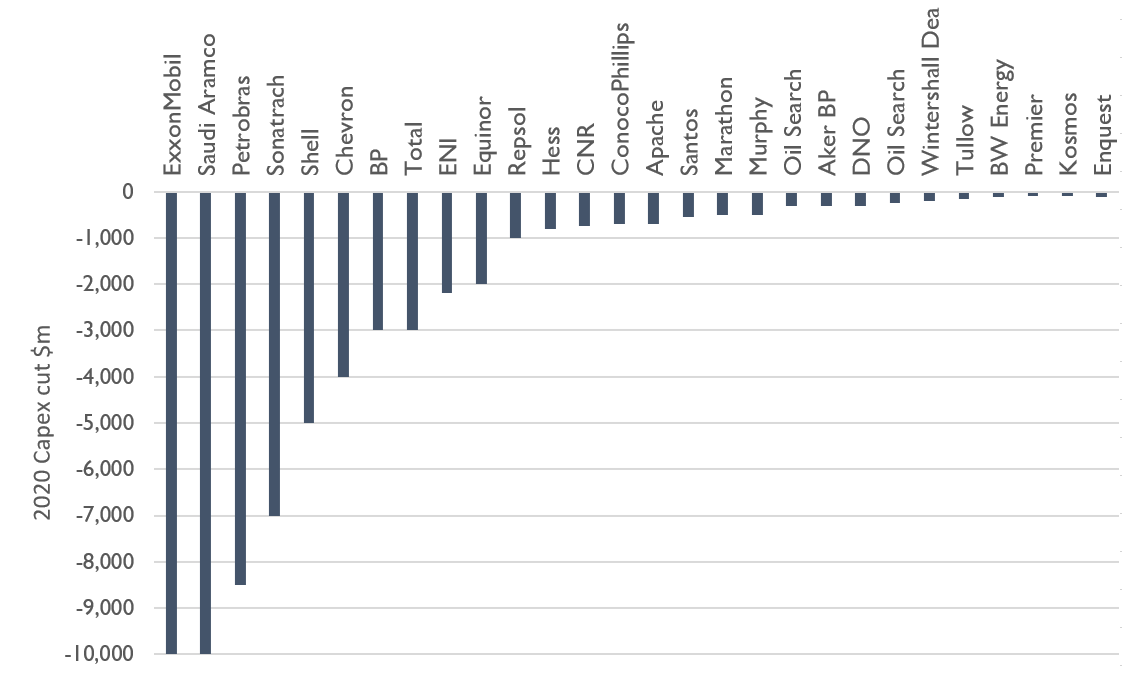

In the last few weeks, oil companies have announced substantial cuts to Capex. The selected companies alongside (selected for their exposure to offshore activity) have cut 2020 budgets on average between 20-30% for the majors and as much as 48% for independents such as Enquest.

Offshore Rotorcraft

What does this mean for offshore rotorcraft activity? Manned production rigs are the beating heart of the offshore crew transfer business and account for more than two-thirds of crew transfer activity. These won’t be hit too hard by the oil price downturn in the short-term but they have seen reduced manning as a result of the coronavirus outbreak this year. Offshore mobile rig activity will undoubtedly take a short-term hit and reduced project sanctioning will also have a short-term impact on rigs and specialist construction vessels working. Speculation has been rife in recent weeks as to the extent of the impact on rotorcraft activity. In the last fortnight the impact has started to become clear in the data we collect.

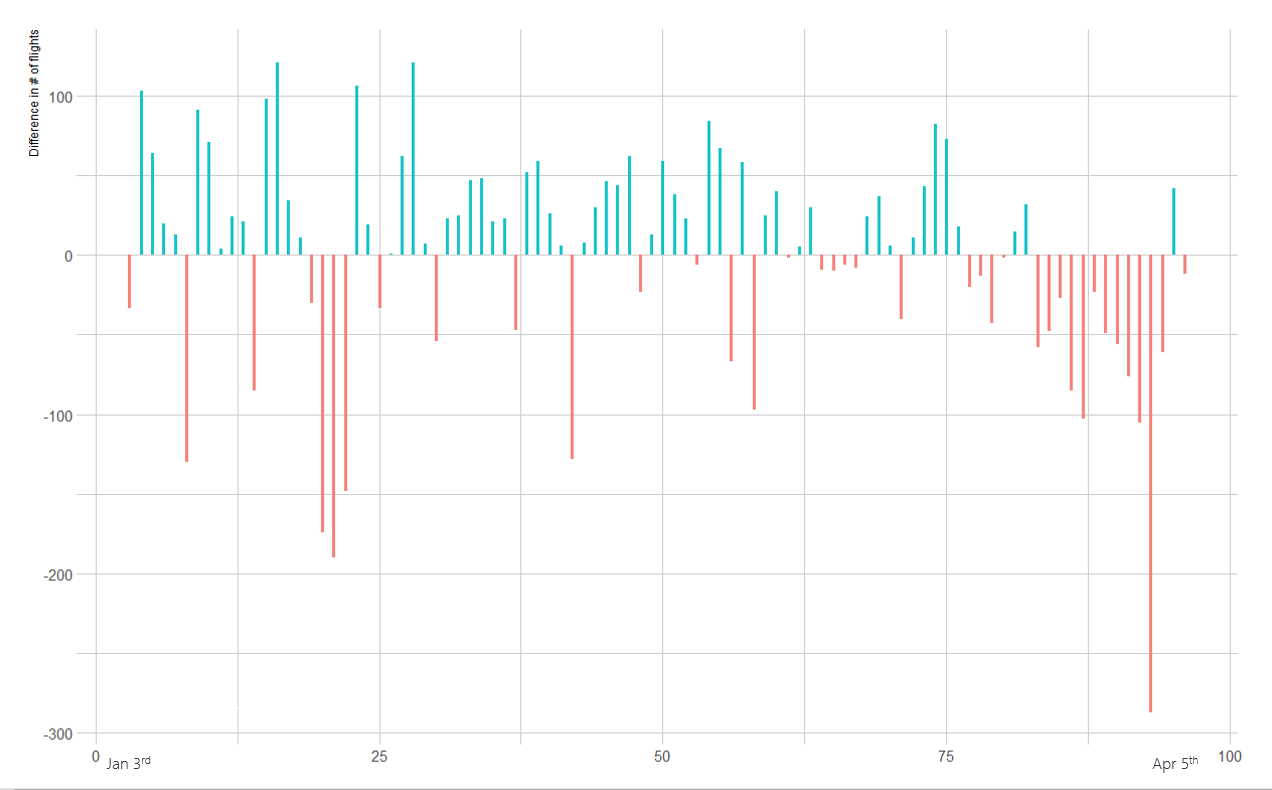

Global: change in flight activity per day year-on-year for Heavy & Super Medium rotorcraft, Jan 3rd - April 5th 2020 vs 2019.

In the chart alongside we show the difference between daily 2020 and 2019 activity for Heavy and Supermedium rotorcraft with positive numbers showing an increase in 2020 vs 2019 and vice versa. The 2020 data are lagged so that weekends and weekdays line up correctly.

We previously showed this chart up to mid-March, at which point there was no measurable impact of Covid-19 measures on the number of flights recorded.

We are now seeing a material impact on offshore crew transfer activty. In some countries the lockdowns are so severe that crews cannot get to work and offshore flights are impossible. In others there have been measures to mitigate coronavirus risks, including reducing manning and increasing spacing between the passengers (that will spend the next three weeks on a rig together) and the helicopter crew. For aircraft such as the AW139 this might mean leaving the first row of seats empty, reducing the maximum capacity of the aircraft from 12 passengers to 8.

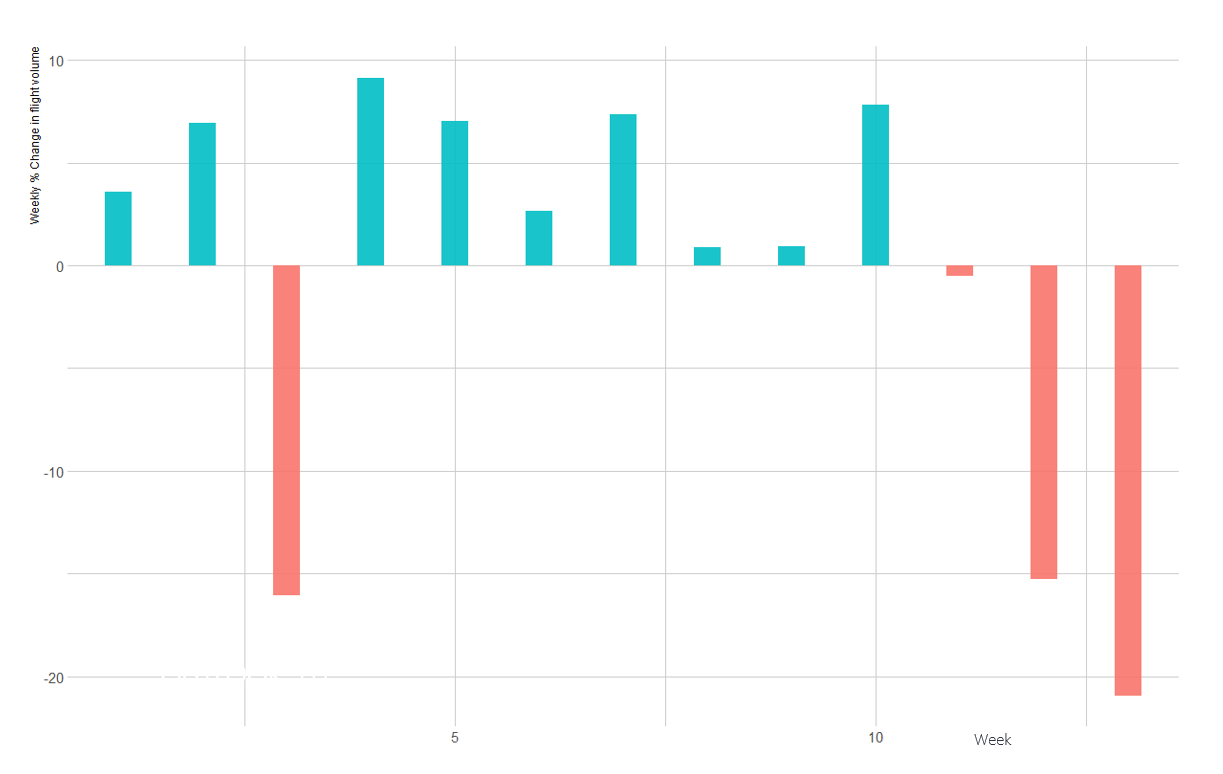

Global % Change in No. of Flights per Week - Heavy & Super Medium Rotorcraft

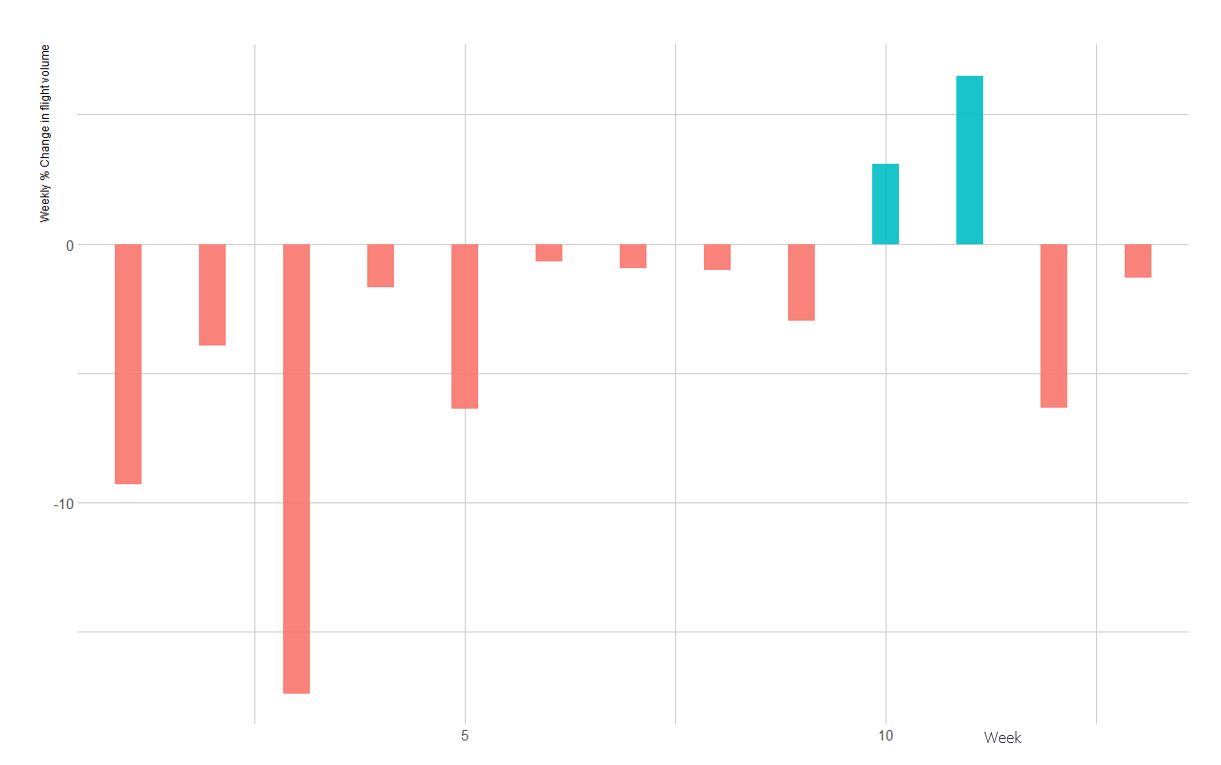

UK % Change in No. of Flights per Week - Heavy & Super Medium Rotorcraft

GLOBAL ACTIVITY DOWN 21% LAST WEEK

Above we show the flight data on a weekly basis, 2020 vs 2019 for heavy and super medium crew transfer rotorcraft. The impact on global activity, left, is clear with a 21% reduction in activity last week vs the same period a year prior. The UK activity is shown on the right hand side. We have seen for most weeks in the first quarter this year a 1-2% lower volume of flights in the UK with weather events that occasionally cause much larger deviations. Despite fewer flights, the UK is not mirroring the global picture in recent weeks. We have seen a slight increase in activity in mid-late March followed by a return to previous levels. Whilst manning offshore in the UK has been decreased it seems this is, for now, off-set by distancing measures and fewer passengers in the aircraft.

Will the OPEC deal change anything in the short term? It won’t change the restrictions in place due to the coronavirus. It’s unlikely the oil companies will change their near-term Capex plans and u-turn on the announced cuts. What it will do, however, is allow the industry to feel slightly more confident about the outlook for what will undoubtedly be a tough few months and perhaps park any suggestion of negative oil prices and complete oil industry meltdown.

Steve Robertson, Director

Air & Sea Analytics