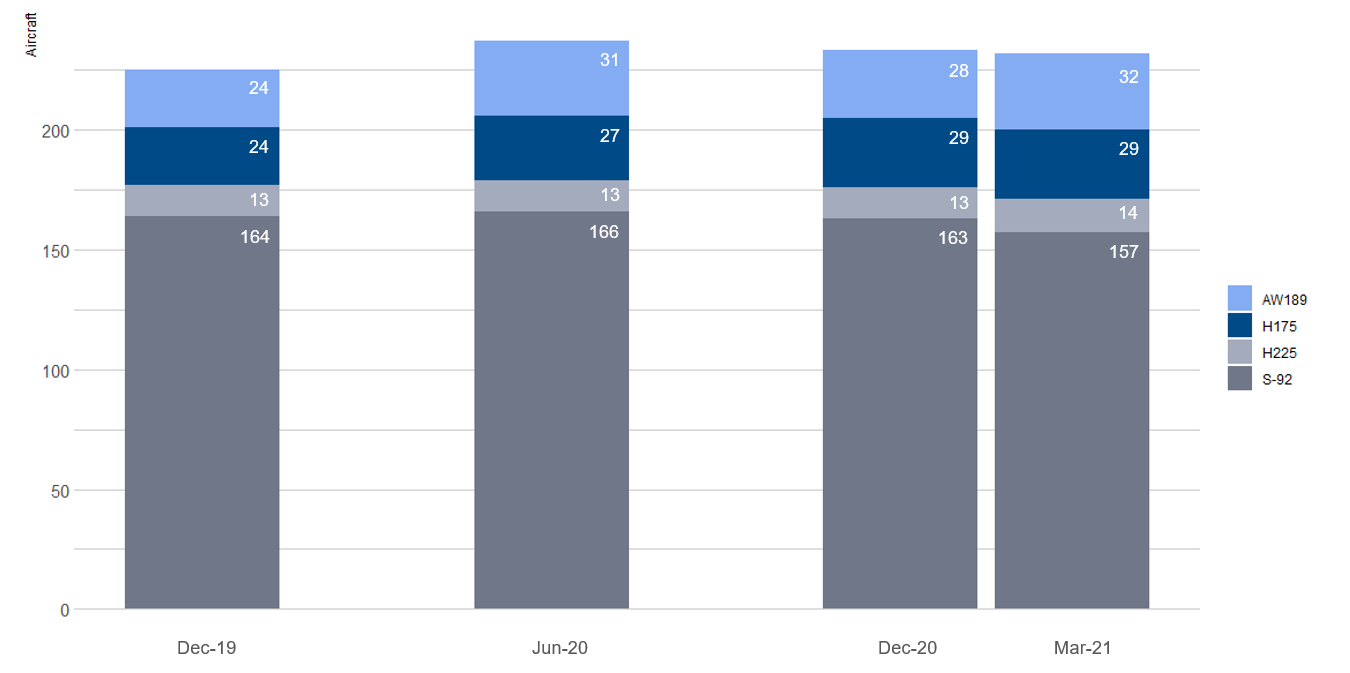

The latest analysis of activity for each S-92 helicopter operating in the offshore crew transfer fleet shows 77% of the fleet were active as of the end of Q1, 2021. A total of eight aircraft were returned to lessors over Q3 and Q4 2020 and a further two were returned in Q1 2021. The active fleet are, in total, flying 10% fewer number of flights now vs January 2020. These are amongst the headline findings of the latest “S-92 Fleet Census” released today by research firm Air & Sea Analytics.

Director Steve Robertson remarked “It was always inevitable that the impact on the active fleet of aircraft would lag the downturn in activity due to the Covid-19 crisis. Flight activity has recovered but remains 10% down on January 2020 levels and subsequently fewer rotorcraft are needed at the present time in this cycle. As of our last census in June 2020, there were 166 crew change S-92s flying and that had fallen to 163 in December 2020 and subsequently to 157 in March 2021.”

We review the fleet unit by unit and share and sense check our outputs on the same basis with the OEM, Lessors and others. The S-92 market has been subject to arbitary speculation for years. The purpose of this analysis is to provide an objective, data-driven, independent view and to evaluate the demand-side (i.e. the number of units flying) rather than cover the supply side (fleet).”

The current market situation can be summarised as a protracted oil industry downturn combined with a global pandemic of a scale not seen for a hundred years. The S-92 remains a mission-critical tool in the oilfield services supply chain and the only heavy helicopter that is accepted worldwide by all of the major oil and gas companies. Given that the drop in utilisation is nothing to do with the utility of the aircraft itself, and is driven by the current market situation, it is reasonable to assume that as the market recovers, S-92 utilisation will also recover. Leading indicators are promising – oil prices have recovered to over $60/bbl, E&P companies are reporting good results in Q1 and as Covid restrictions ease then the business of finding, extracting oil and maintaining the offshore infrastructure can resume properly.”

The ‘S-92 Fleet Census’ report, available now via Air & Sea Analytics, evaluates S-92 usage by country and operator, showing the current position vs previous census. A unit-by-unit breakdown is provided by serial number showing location and status.

A number of operators are thinning their fleets and returning inactive aircraft to lessors. Babcock, Bristow, CHC and Cougar are amongst those returning aircraft. OMNI bucks the trend here, having taken an additional S-92 from Milestone in Q1 2021.

Super-medium units continue to be delivered and find work in the market. We note the success of the H175 in a recent Brazilian tender and also the growing number of H225s being used for crew transfer in China with GDAT supplying aircraft (previously used in the North Sea and Australia) to COHC, the dominant operator with CNOOC. Overall the number of heavy and super-medium units working offshore decreased over the last six months of 2020 from 237 to 233 units and has fallen further in Q1 2021 to 232 aircraft.

For more information please contact us or click on the report cover to the right.