Contract Renewals

A Race to the Bottom?

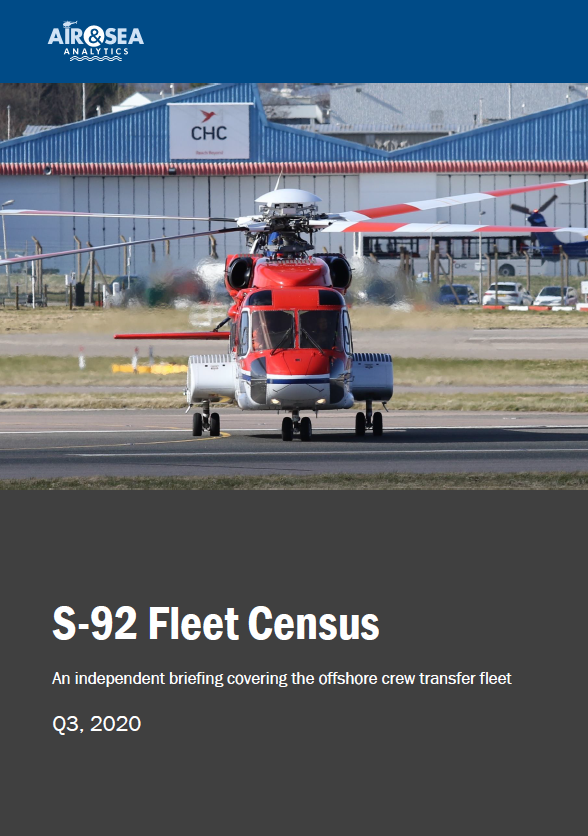

Babcock S-92 G-MCSI taxis to the terminal whilst CHC S-92 G-WNSF departs on runway 23 on a blustery day in Aberdeen, March 11 2020.

The award by oil major Total of two contracts to Babcock, one in Aberdeen (previously CHC) and one in Denmark (previously NHV) has raised eyebrows in the industry and prompted some unusual remarks from CHC last week. Why? Surely it’s not unusual for contracts to change hands between contractor? In this article we walk through the background to the situation and speak to NHV CEO Steffen Bay for his perspective.

HOW DID WE END UP HERE?

Prior to the downturn in 2015, all was essentially rosy in the world of offshore rotorcraft. From an owners’ perspective, assets were holding their value, lease rates were strong with S-92s on contract for north of $250k a month. As an operator, your clients were considered ‘sticky’ and your probability of renewal likely around 90%, so long as you were delivering as expected on the contract.

The oil price downturn changed all of that. As Ed Washecka noted in his interview with us last week, the CHC bankruptcy pushed S-92 lease rates down to $150-200k (and when Bristow and PHI filed for bankruptcy, lease rates were again renegotiated). Oil companies started aggressively renegotiating their contracts with all corners of the oilfield services supply chain and helicopters were no exception. Suddenly contracts were no longer considered ‘sticky’ and fierce price competition led to more-frequent contract switching that we now see as the ‘norm’.

In 2019 Babcock lost several contracts including BP, Spirit, Perenco and went on record saying they would not “engage in a race to the bottom” - Director Simon Meakins spoke to this several times at OEM and public events, making it clear that Babcock would be selective. It all sounded very sensible, and very logical.

Skip forward a few months to February 2020. In a trading update Babcock notes that it will take an impairment on its offshore aviation business of £85 million and states that it will not engage in a race to the bottom offshore and “does not intend to invest further to stay in that market”. A month later it announces a significant contract win - the IAC contract flying primarily to the NNS for Taqa, Enquest and CNR from the Shetlands. Simon Meakins departed in May to head-up a VVIP operation in Saudi Arabia.

June 2020 - Chief Executive Archie Bethel announces the full year results. The write-down in offshore oil and gas jumped to £395 million. If Mr Bethel had been somewhat irritated in February by the oil and gas division he certainly didn’t hold back his frustration in June, stating:

“major problem area continues to be the offshore oil and gas business” “competitors are continuing to bid at lower pricing levels” “When you combine this with the likely impact of Covid-19, we no longer believe this to be an attractive long-term market for Babcock” "[oil and gas] has been frustrating and disappointing and we no longer believe it to be an attractive growth opportunity"

So What’s the Fuss About The Latest Contract?

As noted earlier, contract switching is far more common than it once was. Aberdeen is the busiest offshore heliport in the world and competition between the four players based there (Babcock, Bristow, CHC, NHV) is fierce. Babcock’s decision to go after the Total contract might have seemed a little at-odds with the Chief Executive’s comments in June and February, but they didn’t rule out bidding new work, just noted that they didn’t expect growth.

CHC’s reaction was remarkable, given that usually you would expect there to be no reaction at all. In a notable piece by Mark Lammey at Energyvoice, CHC reacted to the award noting their disappointment and highlighting the “unsustainable pricing”.

Air & Sea Analytics spoke to a person familiar with the contract who said that it was

“marginal for CHC, as it has been renegotiated several times since being signed in 2014”

The Energyvoice article made the further connection between cost cutting measures and compromises to safety. Sour grapes from CHC or did the points raised have merit?

The view from Across the Water

NHV currently operate for Total from Esbjerg in Denmark. Babcock does not currently operate in Denmark and to service the Total contract they will have to incur significant start-up costs including gaining an AOC (Air Operators Certificate- a complex and expensive process) and establishing themselves with hangar and terminal services.

Was there the same view of Babcock in Denmark? We spoke to several persons familiar with the tender who noted that “Babcock undercut [NHV] by a significant amount and with new aircraft” and one going as far as to say “there’s no way they can make money on that contract” and “NHV have flown it for 8 years, they know the geography and jurisdiction very well, they also know the H175 aircraft and the cost of flying it better than anyone having flown 40,000 hours on it recently.” Echoing CHC with a similar point, it was explained:

“This is a new race to the bottom. It’s one thing to low-ball a contract in Aberdeen where you have a presence and aircraft. Doing that in a new jurisdiction is something else. That’s the helicopter business for you. There always one operator who does something destructive like this”

NHV H175 G-NHVE returns to ABZ from the Petrofac FPF1 on March 11, 2020.

The view from NHV

We approached NHV CEO Steffen Bay for comment:

Steffen - you went through the process of getting an AOC recently in the UK. How easy is it?

“It’s a huge effort and its very expensive, I think it’s a little easier in Denmark but it’s still going to cost some significant money, time and effort.“

Can you comment on the speculation re the commercial nature of the new contract?

“No, unfortunately I can’t. What I can say is that Total got what they wanted, even cheaper rates than they already had… Similar to CHC we had to give concessions to Total in the past, so it was not a very profitable contract for us anyway, hence the surprise that Babcock could perform it at even lower rates.”

You were successful winning a contract with Shell recently in the Southern North Sea. We have heard that Shell apply careful diligence in their contracting not just to ensure safe operations but to ensure that the contract isn’t loss-making for the operator and that subsequently there won’t be commercial pressures including commercial pressure to compromise on safety?

“Yes I can confirm that. Shell is doing the right thing, they know what the alternative is. Some companies understand that pushing the operators to the brink of financial collapse is a losing proposition. The major ‘American’ operators already went through a first wave of bankruptcy restructuring, a second one could be devastating.”

This has been described as a new ‘race to the bottom’ - do you think that’s a fair perception of what is happening here?

“I think that’s a fair statement. Despite publicly complaining about low prices, Babcock is now doing exactly what they complained about several months ago, it is a strange game they are playing. Of course, I cannot be sure about their cost structure, but I have participated in enough tenders around the world to know what makes sense financially. In my view this doesn’t. NHV will not participate in a race to the bottom. We will be very selective. We would rather lose a contract than ‘win the right to lose money’ – We are not interested in that.”

“We would rather redeploy the aircraft with customers that appreciate a new, modern aircraft and allow us to make a decent margin. I think that’s legitimate. We are taking significant risk and provide mission critical services that are extremely important to the oil companies. They will have to consider buying the equipment themselves soon, if the current market situation continues. Operators might not be able to finance aircraft anymore, if they cannot make a return. We already see the financial sector pulling back from O&G in general and especially for helicopters it’s getting harder and harder to find funding.”

This is a bump in the road (albeit not without implications for some of your operations) in what has otherwise been a positive year for NHV?

“Of course, we have opened up an additional base in Midden-Zeeland in the Netherlands and we will open up in Blackpool in the last quarter of this year, we have won the SNS Shell contract, extended our Netherlands Search and Rescue Contract, Ithaca extended with us for 5 more years in Aberdeen, the UK business is now our largest business unit with strong double-digit growth in each of the last 4 years and we expect that trend to continue… so yes, plenty of success stories there.”

How is the S-92 market impacting your business?

“Everyone who has an S-92 is heavily discounting them to stay in the market and we are finding that we are competing with these aircraft with our more modern and more capable H175’s… if there was a level playing field where the true cost of the heavies was reflected in the price then it would be different, a lot easier for us for sure. More and more customers are seeing the advantages of the Super Mediums and we are the most experienced operator in that segment, so I am very positive that we will be able to convert this knowledge into commercial success."

Sincere thanks to Steffen for his time and insight.

(We would like to note that in the interests of providing a balanced view we reached out to the appropriate person at Babcock for comment and have not yet received a reply.)

As a reminder, our latest S-92 fleet census was released last week. Providing unit-by-unit detail on current status and location for the offshore crew transfer fleet the report is ideal for stakeholders in the S-92 business and likewise for those that work with competing aircraft. We use state-of-the-art data analytics techniques combined with good old-fashioned primary research to establish who is operating the aircraft, where, and how that has changed. For more detail see here: